Executive Summary

- Politicization continues to rank as the top barrier to scientific progress while scientists place trust in peer-reviewed research, professional networks, and their primary vendors.

- Budget outlooks are improving, yet overall spending remains largely flat, requiring higher output without proportional investment.

- Flat purchasing is not dampening output expectations; productivity is projected to rise, with nearly 90% of scientists expecting to meet their 2026 goals.

- Capital spending focuses primarily on incremental upgrades; novel equipment investments are concentrated in automation and robotics.

- AI and associated techniques/workflows are expected to lead 2026 impact, with automation prioritized amid Biopharma staffing constraints.

In our semi-annual State of Science study, over 450 scientists across the globe told us how they are adapting their priorities, purchasing behavior, and productivity expectations in response to economic and political shifts.

While the global scientific workforce remains cautious, they are no longer defensive. Optimism about scientific productivity is increasing. Budgets are stabilizing. And trust, though concentrated, remains a defining force in scientific decision-making.

Together, these shifts suggest a transition in market dynamics: from contraction and uncertainty toward disciplined expansion and rational purchasing behaviors.

About our respondents

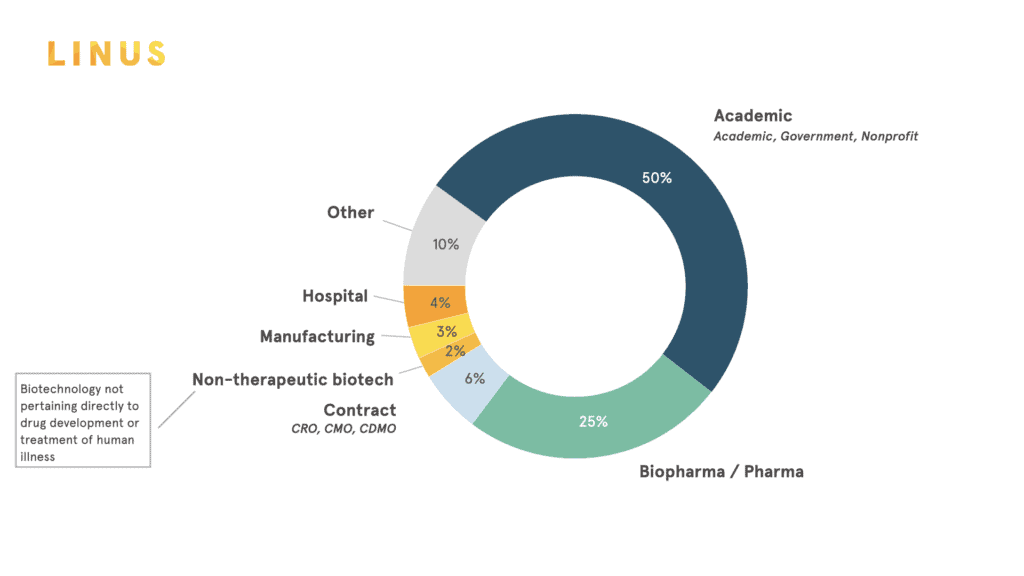

For the 2026 H1 State of Science study, we engaged 455 life science professionals spanning academia, biopharma/pharma, biotech, CRO/CDMO organizations, hospitals, and manufacturing settings. Academia and industry comprise the majority of respondents (50% and 36% respectively), enabling meaningful comparisons between funding-driven research environments and commercially driven organizations.

These findings are informed by respondents in North America (67%) and Europe (23%), with additional representation from APAC (8%) and other global markets.

Q: Which of the following best describes the type of organization you work for or are affiliated with? (n=455)

A Market Rebalancing: Embracing Guarded Stability

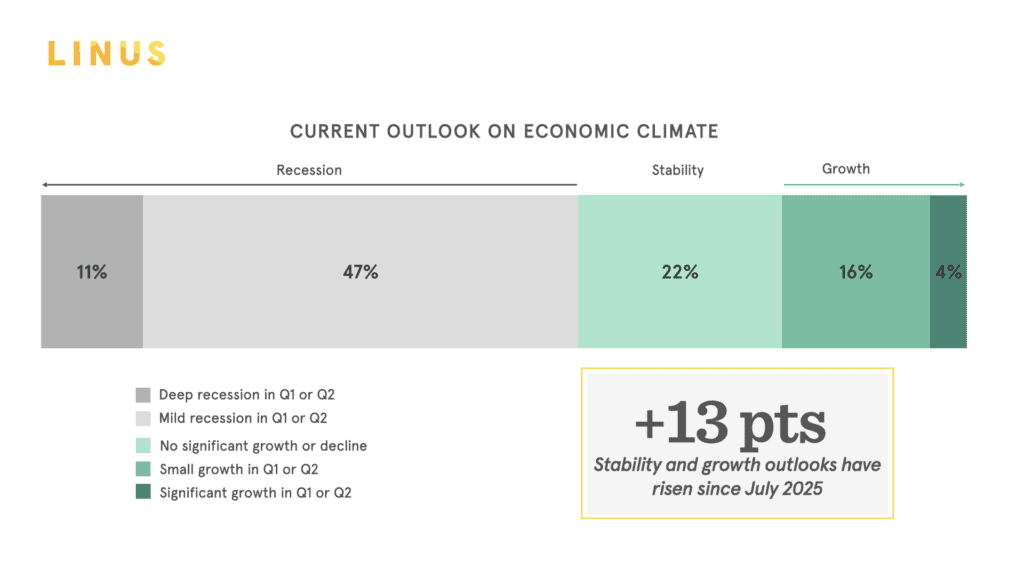

Since our mid-2025 consumer confidence data represented a low-point, economic outlooks have improved, with scientists increasingly expecting stability or modest growth in the first half of 2026. While mild recession expectations remain globally widespread, the sharp pessimism of 2025 is softening.

North America leads in growth expectations (by 5pts), while APAC markets predict relative stability. Biopharma respondents express greater optimism than Academia, particularly regarding small or significant growth scenarios.

Q: What is your current outlook about the economic climate for the first half of 2026?(n=455)

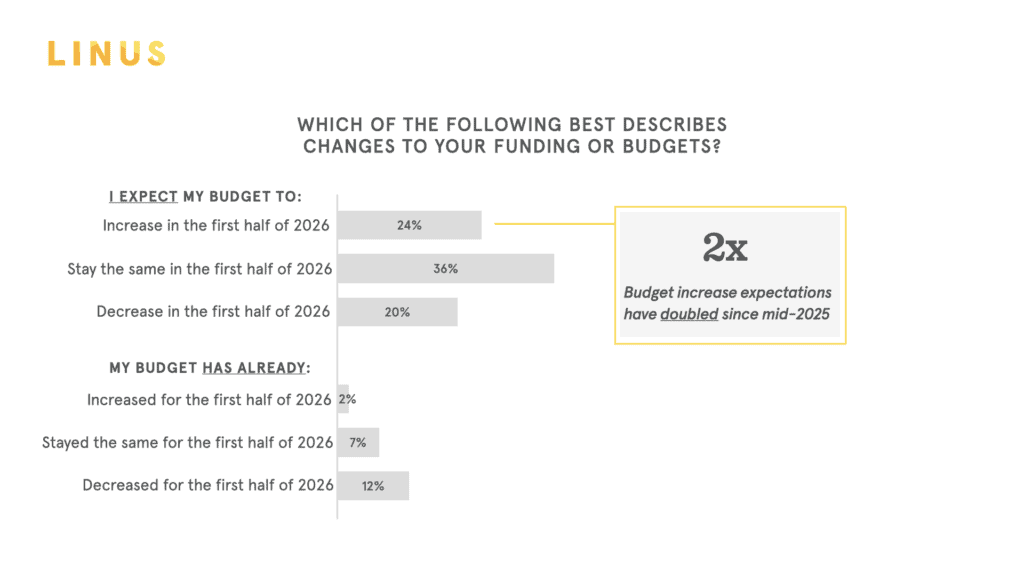

Budgets reflect this cautious improvement. Expectations of budget increases have doubled since mid-2025, yet overall spending is expected to remain largely flat. The current operating environment is defined by a tension between stabilizing outlooks and disciplined spending. Organizations are incrementally regaining confidence while exercising discipline.

Q: Which of the following best describes changes to your own funding or budgets for 2026? (n=455)

Politicization and Trust: The Structural Undercurrent

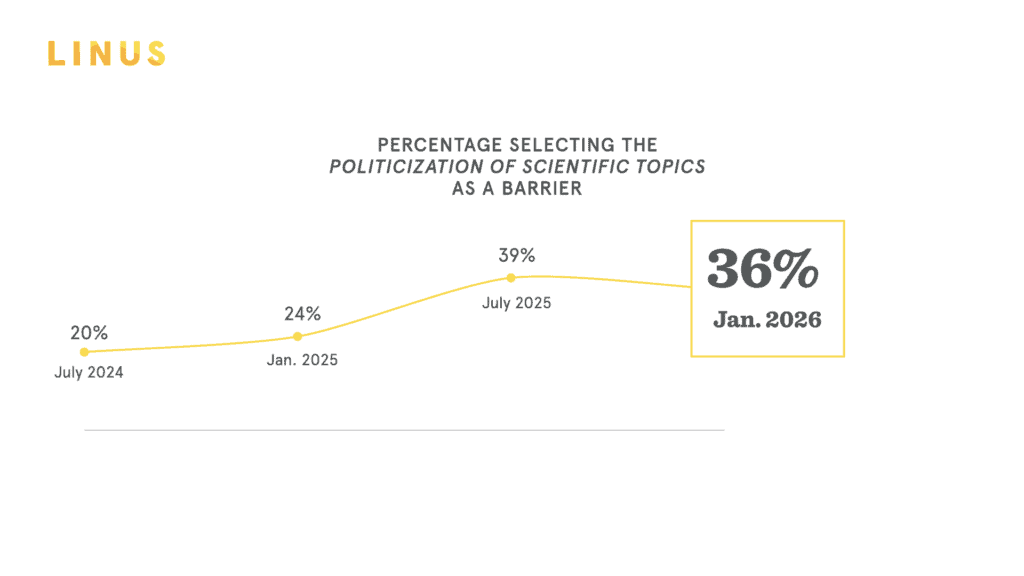

Politicization of scientific topics remains the top barrier in scientific progress, although it was selected less frequently than at any point in the past 18 months. Despite this easing, it continues to shape sentiment.

Q: In your opinion, which of the below are the top 3 barriers in life science today? (n=455)

As the politicalization of science is a persistent barrier, 85% of scientists focus their trust on peer-reviewed publications and almost 60% focus on professional networks. Scientists report significantly higher trust in those within their own communities (almost 55%) versus outside them (less than 35%).

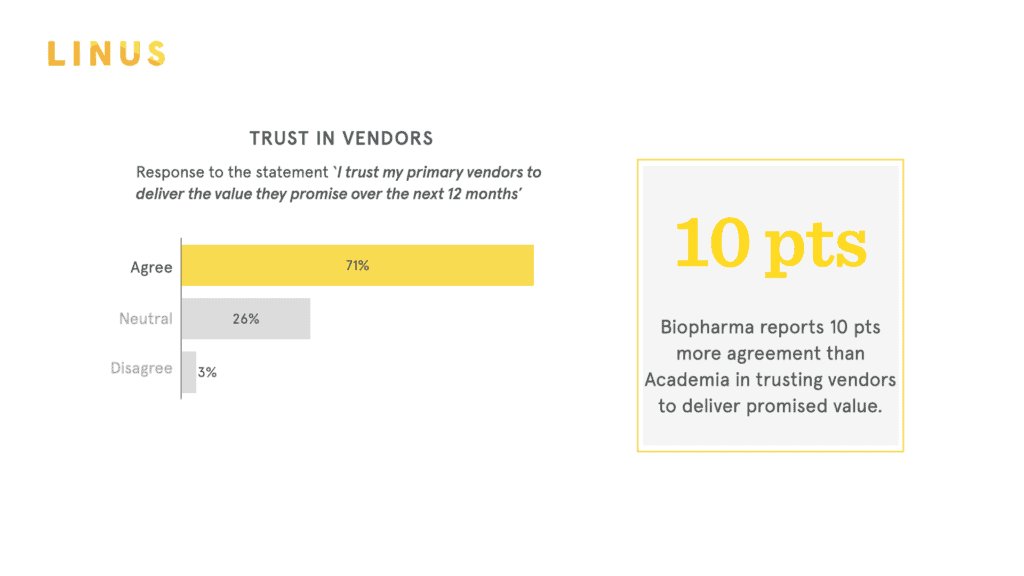

Encouragingly for vendors, over 70% of scientists agree they trust their primary vendors to deliver promised value in the next 12 months. This trust is anchored in longstanding relationships, reliable performance, and strong technical support.

Takeaway: Vendors who embed themselves in scientific communities and demonstrate defensible value are advantaged over those relying on brand recognition alone.

Q: How much do you agree with the statement below? ‘I trust my primary vendors to deliver the value they promise over the next 12 months’? (n=455)

Purchasing Behavior: Focused Upgrades

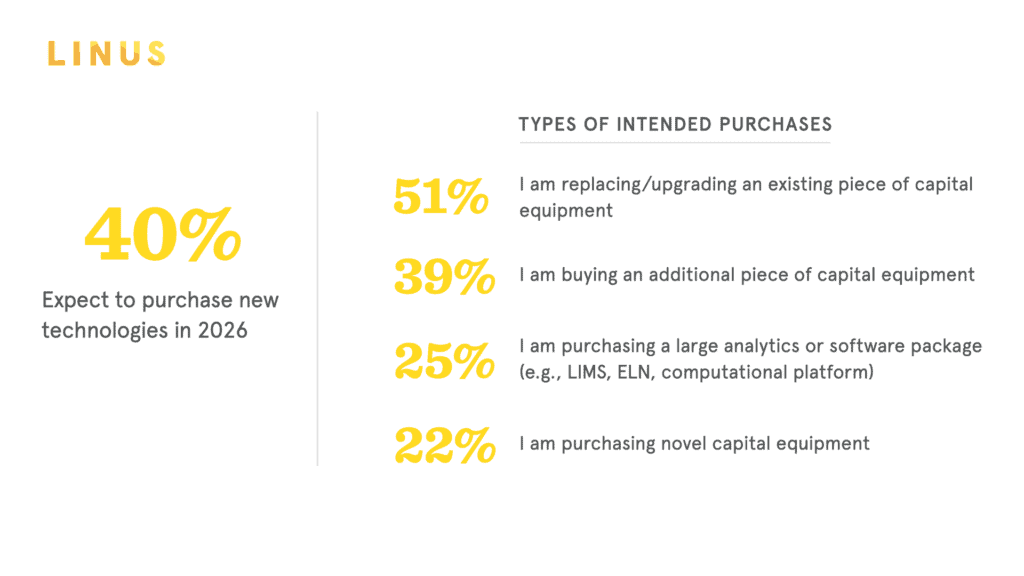

Purchasing behavior remains steady. Intent to purchase new technologies remains largely unchanged from late 2025 levels. Among those planning purchases, 51% are replacing or upgrading existing capital equipment rather than investing in net-new expansion.

Q: Which of the following best describe the technologies you plan to purchase in the first half of 2026? (n=183)

Automation and robotics lead as the top category for novel capital investment. Meanwhile, 85% of scientists expect to maintain or increase purchasing of reagents and everyday lab products.

When excluding funding, the primary barriers to purchasing are internal alignment (18%) and expertise gaps (13%) — not demand. Staffing constraints are particularly influential in Biopharma, reinforcing automation as a productivity lever.

Takeaway: Capital deployment is selective. Organizations are prioritizing technologies that increase throughput, reduce operational friction, and produce measurable gains without adding headcount.

As Consumer Confidence Grows, Productivity Expectations Climb

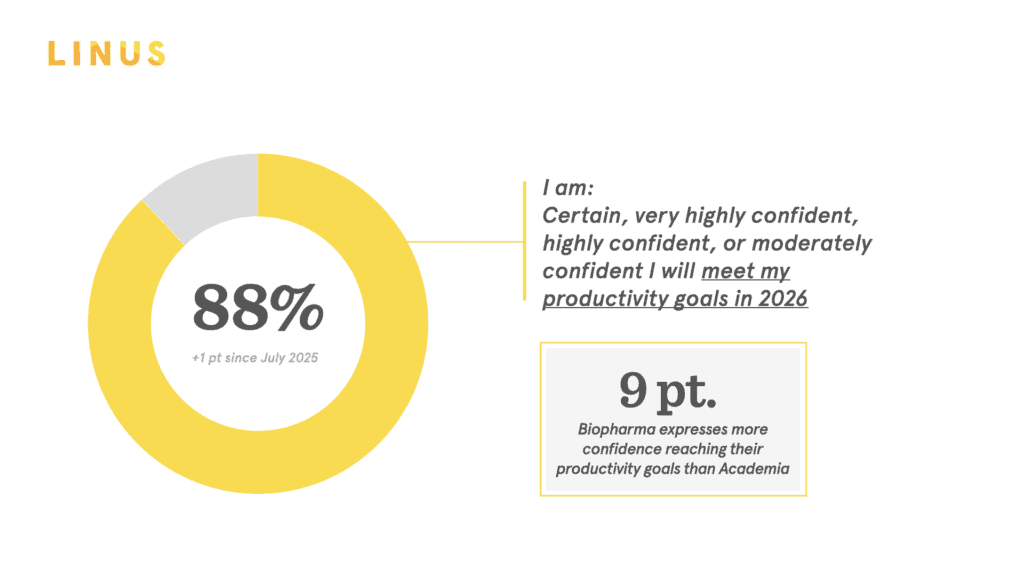

Despite economic caution, productivity expectations are rising. Nearly 90% of scientists say they will meet their productivity goals in 2026, and 42% expect elevated productivity rates in the coming six months.

Q: Overall, how confident do you feel that you will meet your target productivity goals or intentions in the first half of 2026?

Biopharma respondents are particularly optimistic, with approximately half expecting higher productivity levels. Across geographies, over 40% of teams project increased output.

Scientists expect the most impactful technologies in 2026 will be AI enabled bioinformatics (32%), and generative AI for structure prediction (28%). However, almost 20% see automation and robotics to be highly impactful.

Takeaway: The industry is preparing to deliver more output with comparable or only modestly increased investment.

2026 Expectations: AI and Funding Take Center Stage

AI-enabled bioinformatics and generative AI remain the techniques predicted to have the most significant impact in 2026. Adoption of machine learning and AI ranks among the top three priorities entering the year.

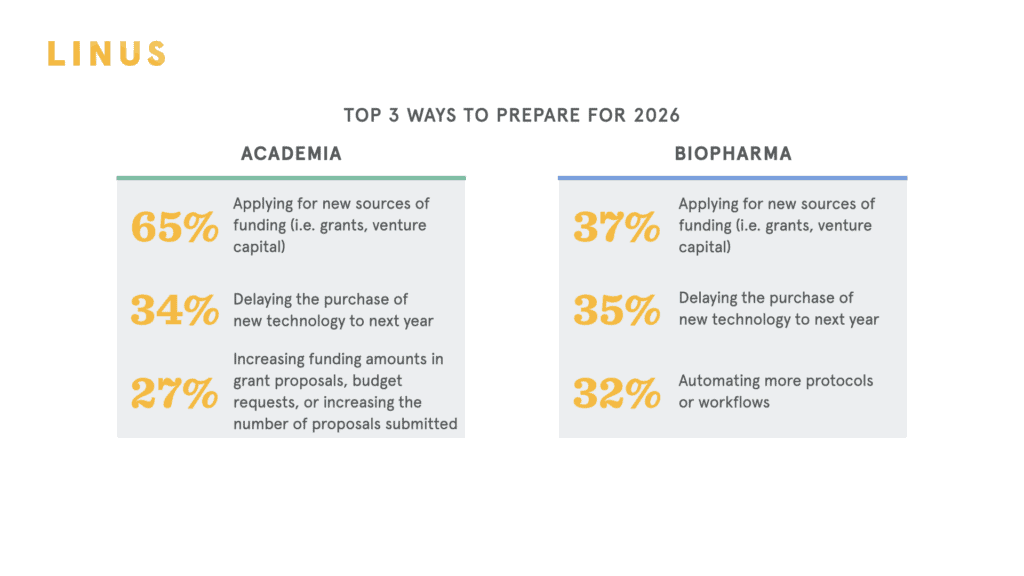

At the same time, 50% of scientists cite applying for new funding sources as a top preparation for 2026, with Academia heavily focused on grants and Biopharma balancing funding pursuits with operational automation.

Takeaway: AI is not being pursued as experimentation — it is being adopted as a productivity instrument. Funding diversification and operational optimization will define competitive advantage in 2026.

Q: Please select the top 3 ways you are currently preparing for the first half of 2026 given your economic outlook for the next 6 months. (n=455)

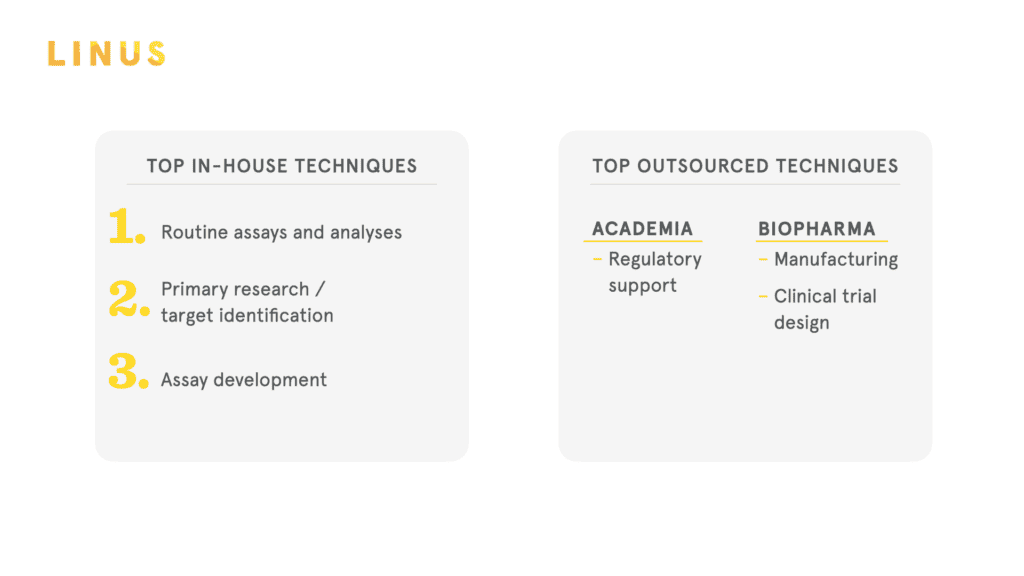

Q: Which of the following are you planning to bring in-house in the first half of 2026? Q: Which of the following are you planning to outsource in the first half of 2026? (n=455)

What This Means for the Industry

The State of Science in 2026 reflects resilience, discipline, and a recalibration toward performance-driven growth.

The 2026 State of Science is defined by three major themes:

1. More positive outlook, not full recovery

Recession expectations have eased but confidence remains measured.

2. Steady purchasing with added emphasis on automation

Capital is flowing toward incremental upgrades and throughput-enhancing technologies.

3. Rising productivity without proportional spend

Scientists expect increased output despite flat or disciplined budgets.

For vendors and industry leaders, the implication is clear: measurable productivity impact matters more than narrative positioning. Organizations are not expanding recklessly—they are optimizing deliberately.

Would you like to receive the above figures in a slide format? Need specific insights about your particular audience or techniques? We’d be happy to connect — contact us! hello@thelinusgroup.com