SUMMARY

- The perceptions, or ‘consumer sentiment’ of scientists shapes their behavior, including their purchase intent. Understanding perceptions is a key indicator of purchase intent from consumers of life science offerings.

- The outlook for productivity in 2023 is optimistic, where 53% expect their baseline of productivity to be somewhat or significantly higher

- Scientists are prioritizing adoption of new techniques to acquire new types of data. Nearly 70% of respondents say they will purchase new technology in 2023.

- For the first time, AI and machine learning are seen as a top priority for their impact in life science. To prepare for the economic downturn, scientists are taking measures to increase their productivity through AI, automation, and in-sourcing.

In today’s fast-changing current economic climate, we may be able to strategically plan priorities for the next year that will require life science executives to stay close to how their customers are thinking and feeling. Our semi-annual State of Science survey reveals how scientists around the globe continue to adapt their priorities, productivity, and mindset — and how that may affect the techniques they use, the products and services they purchase, and the labor force they require.

As 2023 gets underway, we found a heightened interest in how the economic outlook may impact the life science industry. We measured whether scientists are anticipating economic growth or a downturn, and the specific actions they are taking to protect their scientific progress and their productivity in these scenarios.

About Our Advisory Respondents

Using our digital research platform, we surveyed 170 scientists working across multiple geographies, organizations, applications and levels of responsibility. In total, this group represents a directional sample for the industry. This survey is mainly composed of scientists from North America (48%) and Europe (36%), with the remainder working in the rest of the world.

Nearly one-third (29%) of respondents work in an academic research setting and another 28% of respondents work in pharmaceutical and biopharmaceutical research or development. The remaining half of the respondents make up a spectrum of related research and development activities, in services, industrial biotechnology, manufacturing, or clinical applications.

Nearly 30% of our respondents use techniques usingin antibody based protein detection, 24% routinely use PCR, and another 23% work with animal models. This suggests that our cohort is predominantly interested in cell function and cell-based techniques.

Scientific Priorities

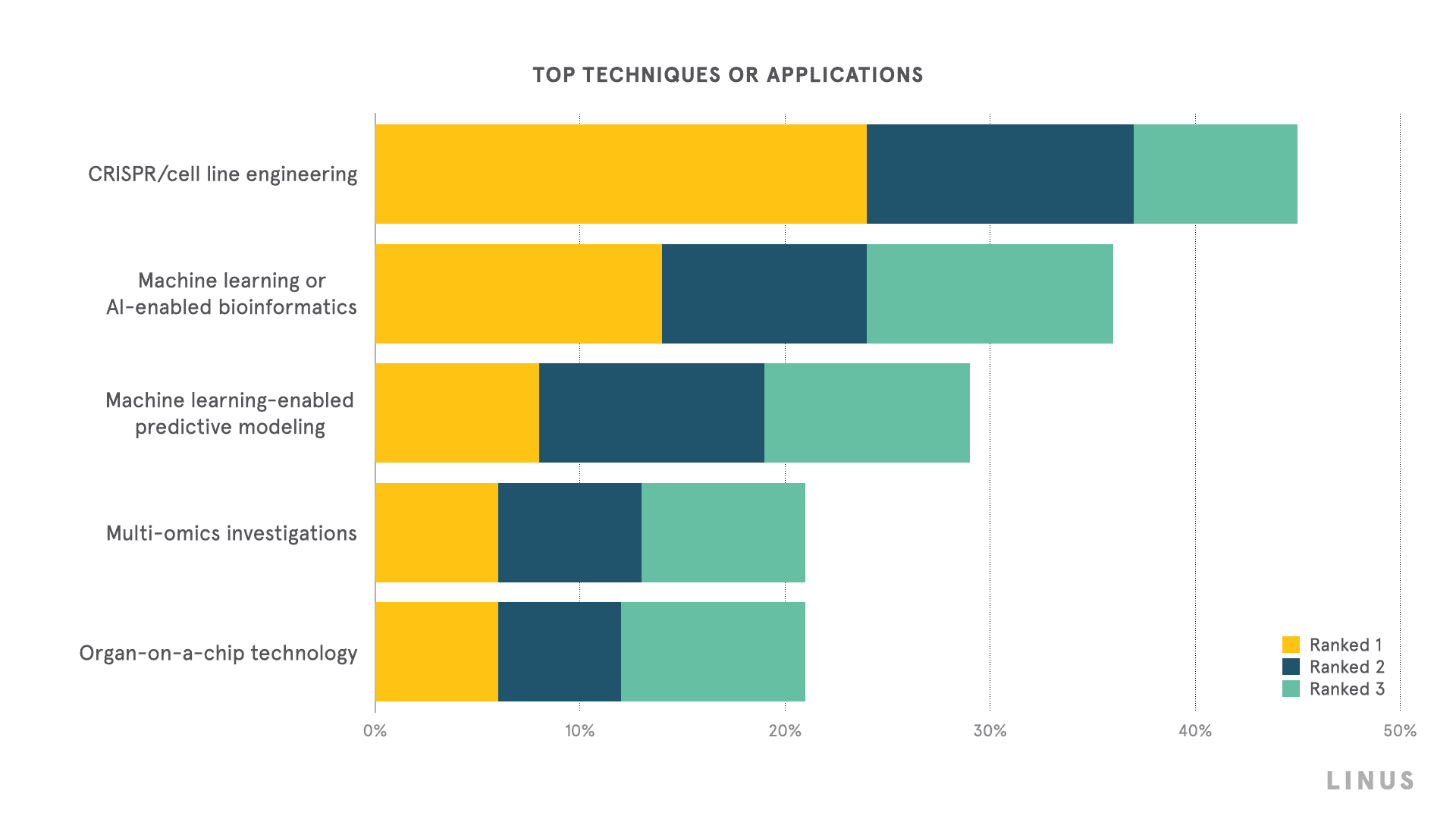

To understand which techniques or applications will be most impactful to science in 2023, we asked respondents to rank what they believe will make the most significant contribution to scientific research.

CRISPR/cell line engineering, machine learning or AI-enabled informatics, and machine learning-enabled predictive modeling will make the most significant contributions to scientific advancement in the next year. In 2022, respondents identified CRISPR/cell line engineering and AI as the techniques that would make the most impact, but for the first time, we see predictive modeling is not seen as mature enough to make significant impact to science in 2023.

In previous surveys, we had found that multi-omics and long read sequencing occupy the list of top techniques. The progression of AI is already dominating conversations of 2023, increasing its relevance in this survey.

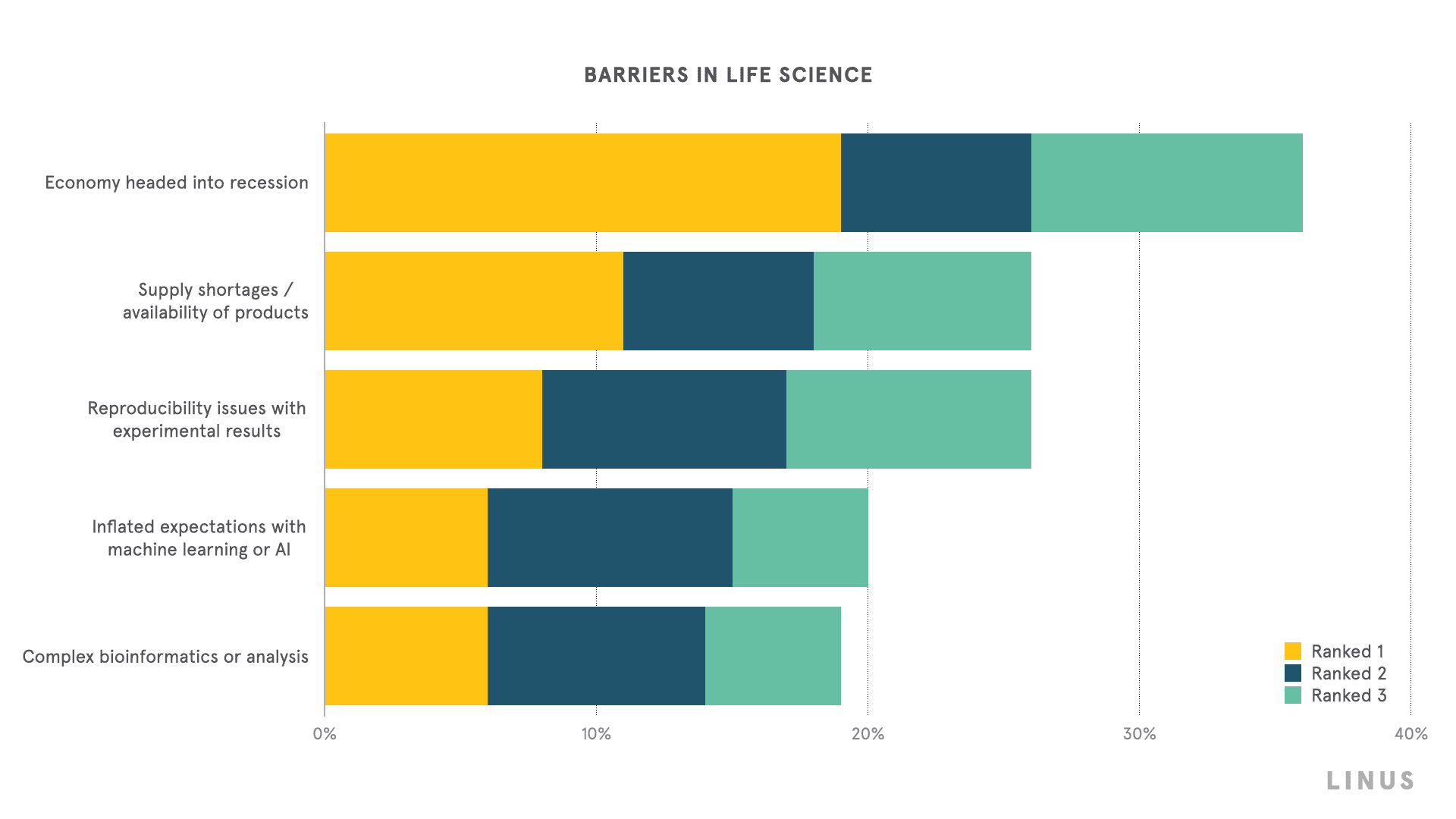

Another major change that we recorded is the anticipated economic outlook in 2023. Scientists believe a potential recession will constrict progress in life sciences, which in turn, could be contributing to their worries about supply chain issues. Concern with reproducibility has fallen from the top concern and replaced with supply shortages and availability of products. Also worth noting is the prominence of inflated expectations with machine learning or AI, which in prior years had been seen as a middling barrier to progress.

Measuring productivity

Overall, we found that the outlook for productivity in 2023 is optimistic. Even in the face of economic and supply chain headwinds, 79% of scientists believe their productivity will not decrease in 2023 from pre-pandemic levels. More than half (53%) of respondents anticipate higher productivity, compared to the pre-pandemic year of 2019.

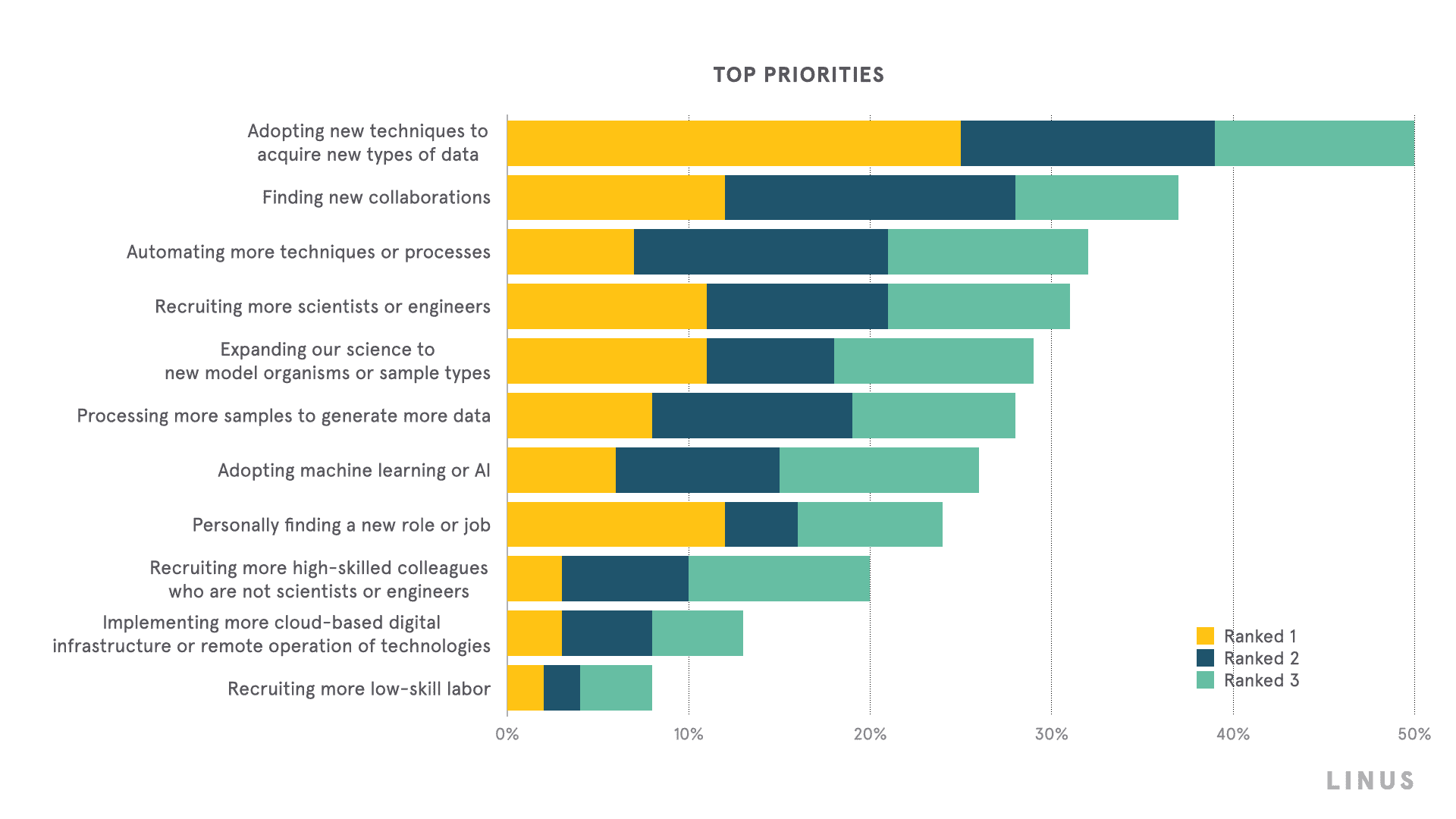

Just as in 2022, scientists are prioritizing technology adoption, collaboration, and automation in their 2023 work. These priorities show that scientists are optimistic to forge paths toward creating novel data and making progress in their scientific endeavors.

Our advisory respondents’ measurement metrics for productivity are more dispersed than in 2022, which suggests that they are now more concerned about ensuring forward momentum than before. The percentage of respondents who gauge their productivity with pre-determined milestones has fallen by more than half: from 65% to 31%. Significantly more scientists are now focusing on objective measures of productivity such as number of experiments and funding received when compared to last year’s sentiments.

For academia, these productivity metrics vary somewhat in which they are more concerned about impact factor of publications and number of publications.

For those of our respondents who anticipate lower productivity than pre-pandemic norms, labor and sample shortages are cited as the main reasons: inability to access labs, limits in training new recruits, or access human samples to a lack of staff or resources being diverted to personnel, and funding

For the scientists who anticipate higher productivity, adaptable workplaces, the quality of collaborations, artificial intelligence, and automation were cited as the main drivers.

Technology Purchases

For 2023, most respondents plan to purchase new technology — a drastic change from our findings in mid-2022, when only 32% of scientists stated they intended to purchase new technologies in the remainder of the year. Starting 2023, the numbers have reversed, with two out of every three respondents planning to purchase new technology. Of that technology, we found that sequencing and different types of spectrometry (LC/MS, GC/MS, etc…) lead in purchase intent.

Almost half of respondents who do not plan to purchase new technologies cite lack of funding as the primary driver. Beyond finances, many of the 32% of scientists who do not plan to purchase new technology report having recently purchased new technologies, virtually eliminating their need to purchase new tools.

Unsurprisingly, it was confirmed that academic scientists are more likely to be impacted by finances, where over half (52%) said their lack of funding impacts their purchasing intent. Of our respondents in industry settings, only 38% identified funding as the culprit to lack of purchase intent.

Economic climate

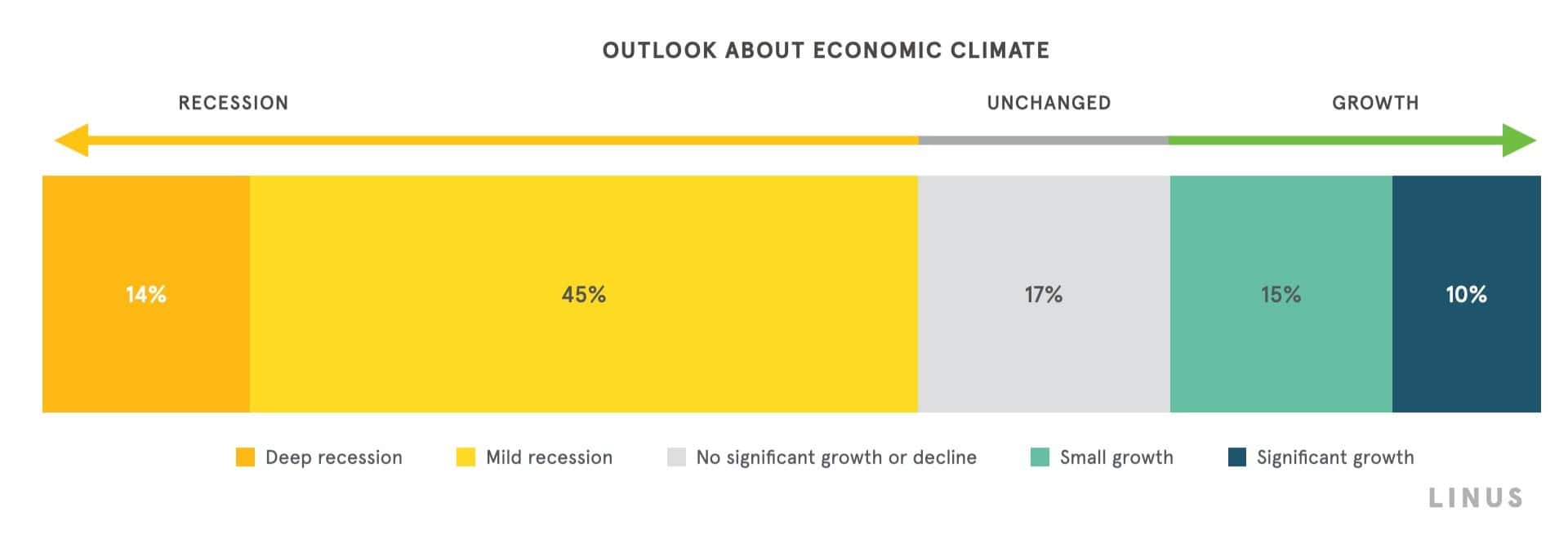

The perception of an economic downturn is bound to have an impact on the life science industry. We found that 45% of scientists are preparing for a mild recession in 2023, in contrast with another quarter who believe the economy will grow. Another 17% of scientists’ outlooks remain unchanged. Of those who do anticipate an economic change in 2023, 52% predict the change will happen in the first half of 2023, but will be short lived, with 41% anticipating that it will merely last throughout 2023, another 54% predicting a 1-3 year cycle and only 5% anticipate it will last for 3 to 5 years.

Despite these outlooks, scientists predict that they won’t foresee severe budget changes in 2023. 76% of respondents fall between a chance of -20 to +20 percentages of change to their budget. Overall, academic scientists predict more budget growth on average. By calculating the mean of the budget changes, we see a slight next increase of +4.4%, which does not keep pace with the 2022 inflation.

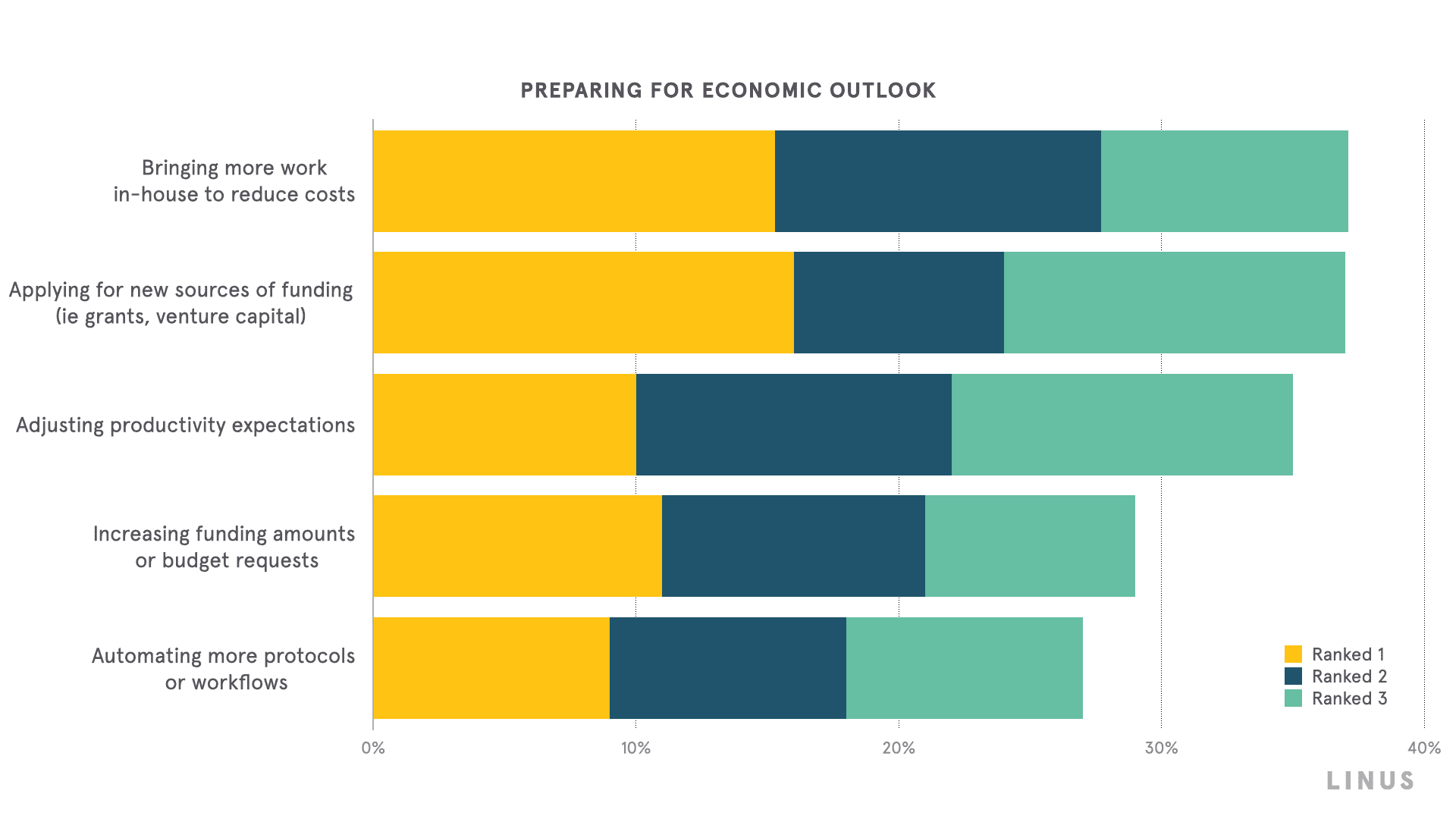

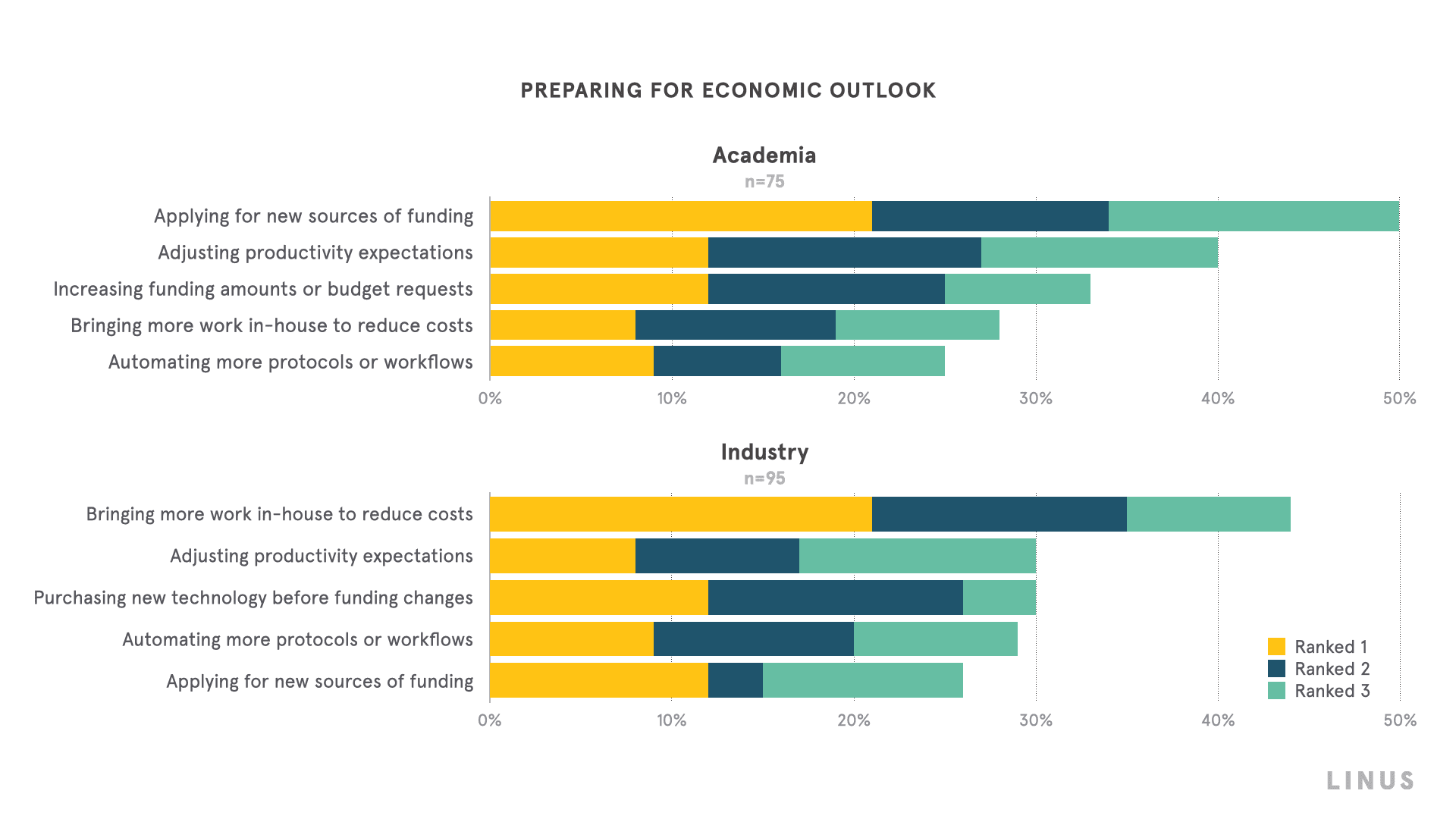

We also found that the 2023 economic outlook inspires proactivity and may be acting as a motivator in the scientific community. Scientists want to take control, citing their intent to change approaches in outsourcing and productivity while expanding funding resources.

One significant difference between scientists in academia and scientists in industry is how they’re preparing for 2023. While both groups plan to insource work to reduce costs and to increase their budget requests, we found that industry scientists are preemptively purchasing technology early in the year before funding changes.

Summary

The ‘consumer sentiment’ of our advisory respondents leads us to believe that they are heading into 2023 with an aggressive stance toward their own productivity despite anticipating a recession.

While we see an underlying thread about labor, our advisory respondents intend to increase their productivity through the use of automation, collaborations, and machine learning technologies.

Scientists in academia are increasing their efforts in funding applications, while adjusting their expectations and milestones, while their industry colleagues are planning to insource activities and making technology purchases before funding changes.

Overall, we gain a sense of optimism within the industry. While the COVID-19 pandemic generated surplus revenues for many players within the industry, any pandemic-driven barriers to productivity seem to have subsided and scientists have taken the opportunity to create efficiencies that they look to leverage in 2023 with all of the chances that the coming year lays ahead for the industry.